4 in 5 Canadians say housing crisis is shaping life decisions, survey finds

Homeownership is becoming a pipe dream for many Canadians, according to a new survey released by Habitat for Humanity Canada. Four in five Canadians now say that buying a home feels like a luxury, while 88 per cent of renters say the goal of owning a home in Canada has become out of reach. The organization’s third annual affordable housing survey looked at the broader implications of Canada’s housing crisis. An overwhelming 82 per cent of Canadians voiced deep concern over how the housing crisis is impacting health and well-being, while 78 per cent see homeownership as a critical factor in the country’s growing wealth gap. The findings show a clear, collective anxiety across generations, with younger Canadians bearing the brunt of housing-related challenges. “Canadians are sending a clear message: the housing crisis is no longer just about housing,” says Pedro Barata, CEO of Habitat for Humanity Canada. The shrinking middle class Survey data reveals concern that the scarcity of affordable housing is fragmenting communities and threatening the middle class, with 82 per cent of respondents worried about a potential decline in this socioeconomic group. Over half of Canadians report worrying about sacrificing essentials like food, education and living expenses to cover their housing costs. Meanwhile, 41 per cent of respondents say the stress alone of not being able to buy a home is difficult for them to manage. Younger generations forced to rethink milestones Canada’s housing crisis is causing younger generations to rethink life plans. Two-thirds of Gen Z Canadians and almost half of Millennials have considered delaying starting a family because they can’t afford a suitable home, while four in ten say they have fewer job opportunities because they had to move to a more affordable area. A notable percentage (29 per cent of Millennials and 25 per cent of Gen Z) say they would consider moving abroad to find affordable housing. The survey also reveals that 73 per cent of Gen Z respondents are anxious about saving enough for a down payment. Barata emphasizes that young Canadians rethinking or delaying major life decisions could lead to “a deep and lasting impact on future generations and society as a whole.” Despite the mounting challenges, Canadians overwhelmingly support the idea of homeownership, with 87 per cent believing it offers stability, and 81 per cent seeing it as a way to build a better future for their children. Calls for action As Canada’s housing crisis grows, the survey reveals a clear demand for political action. Seventy-five percent of Canadians believe that housing policy should transcend political divides, urging a unified approach to the crisis. However, 68 per cent are skeptical that the federal government will reach its goal of building 3.87 million new homes by 2031. Canadians want policy initiatives that reduce taxes and fees for first-time buyers, promote affordable homeownership and convert unused spaces into housing. “Homeownership can’t just be the privilege of the wealthy or lucky few,” says Barata. “At Habitat we see the transformational change that happens when families own their own home, affordably. The security and peace of mind benefit their health, economic opportunities and investments in their community. It benefits all of us.”

Bank of Canada Cuts Interest Rates to 3.75%: Reduction of 50 Basis Points

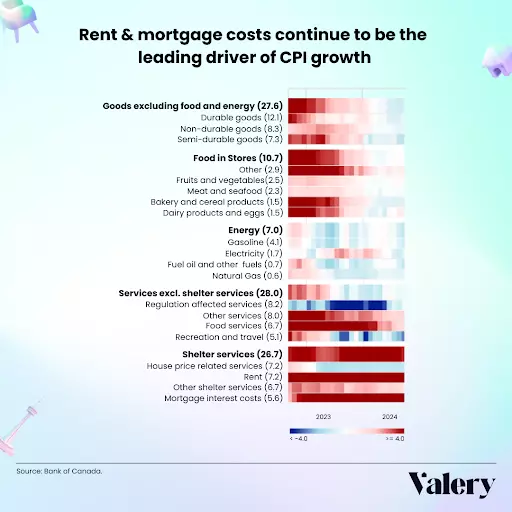

On October 23, 2024, the Bank of Canada cut its key interest rate by 50 basis points, as many experts were predicting, lowering the overnight rate to 3.75%. The Bank Rate now stands at 4%, and the deposit rate matches the overnight rate at 3.75%. This move aims to support economic growth while maintaining inflation close to the Bank’s 2% target.Source: Bank of CanadaEconomic Background for the AnnouncementGlobally, the Bank expects the economy to grow by about 3% over the next two years. Growth in the U.S. is projected to be stronger than earlier predictions, while China’s outlook remains sluggish. The eurozone is experiencing slow growth but is expected to recover slightly next year. Inflation in advanced economies has eased and now hovers near central bank targets. Global financial conditions have also improved since July, partly due to expectations of lower interest rates. Oil prices have fallen by $10 per barrel since the Bank’s July Monetary Policy Report.In Canada, the economy grew by 2% in the first half of the year and is expected to slow slightly to 1.75% for the remainder of 2024. While consumer spending has increased, it is declining on a per-person basis. The labour market remains soft, with unemployment at 6.5% in September. Although population growth is expanding the labour force, hiring remains modest, especially affecting young people and newcomers. Wage growth continues to outpace productivity gains, contributing to an economy operating with excess supply.Looking ahead, GDP growth is expected to strengthen, driven by lower interest rates and increased consumer spending per capita. Residential investment is forecast to rise, fueled by high demand for housing and increased spending on renovations. Business investment is also predicted to pick up, while exports remain strong due to robust U.S. demand. The Bank projects GDP growth of 1.2% for 2024, increasing to 2.1% in 2025 and 2.3% in 2026.Inflation has dropped significantly, from 2.7% in June to 1.6% in September. Shelter costs, while still high, have started to ease. Global factors such as lower oil prices have reduced inflationary pressures on gasoline, contributing to the overall decline. The Bank’s core inflation measures are now below 2.5%, and inflation expectations among businesses and consumers have largely returned to normal.Forecast and Future ActionsThe Bank expects inflation to stay close to its 2% target in the coming years. While shelter and services continue to exert some upward pressure, this is expected to lessen. As the economy absorbs excess supply, inflationary pressures should remain balanced.With inflation now near the target, the Bank reduced its policy rate to stimulate economic growth. The Governing Council hinted at the possibility of further rate cuts if the economy evolves as forecast, but any future decisions will depend on new data and its impact on inflation expectations. The next interest rate announcement is scheduled for December 11, 2024, with a full economic outlook to be published on January 29, 2025.

The Impact of Social or Affordable Housing on Nearby Housing and Investment Properties

Social or affordable housing is designed to provide accommodation for individuals and families who cannot afford market-rate housing. In Canada, the development of these types of housing has become increasingly relevant as cities grapple with rising real estate prices and a growing need for affordable living options. A key area of concern for real estate investors is the impact of social housing developments on nearby property values. Perception vs. Reality: Social or Affordable Housing and Property ValuesMany people share the perception that affordable housing negatively impacts property values. However, multiple studies challenge this belief. The National Bureau of Economic Research finds little to no consistent negative impact on home values near affordable housing projects, especially in urban areas where housing supply is constrained. In fact, certain affordable housing developments have revitalized underdeveloped areas, contributing to property value appreciation.In Canada, the CMHC highlights several examples where affordable housing projects have improved neighbourhood conditions, stabilizing or even raising property values. In some cases, supportive housing projects also introduce community improvements, such as upgraded infrastructure, which can enhance the appeal of nearby properties.Factors Affecting Property Values Near Social or Affordable HousingNot all neighbourhoods are impacted equally by social or affordable housing developments. A report by Civida in 2021 identifies key factors that determine whether property values will increase, decrease, or remain stable near such projects.Design and IntegrationAffordable housing projects that integrate well with existing architecture and community aesthetics face less stigma. High-quality design and construction often result in a positive impact on nearby property values, as these developments are seen as enhancing the neighbourhood.LocationProximity to amenities like schools, parks, and public transit is a critical factor. Affordable housing in high-demand areas tends to have a neutral or even positive effect on surrounding property values, while projects in lower-demand areas may face more challenges.Pre-existing Neighbourhood ConditionsAffordable housing in declining areas can help revitalize the community, leading to rising property values. In contrast, in stable or affluent neighbourhoods, property values may appreciate more slowly, though a decrease in values is rare.Local Policy and SupportCities that prioritize community consultation and ensure affordable housing projects are well-planned and supported by local services tend to see better outcomes. Research from the Furman Center shows that well-managed affordable housing developments, backed by proper oversight and funding, can lead to neutral or positive impacts on surrounding property values.Risk or Opportunity?For investors, affordable housing may initially seem like a risk to property values, but the reality is often more complex. The impact of well-designed, integrated affordable housing is often neutral or positive, especially when developments align with the needs of the community and improve local infrastructure. Real Estate Economics suggests that in strong housing markets, these developments can offer unique investment opportunities. Public investments in infrastructure and services typically accompany affordable housing projects, enhancing the area’s long-term appeal and potential for growth.Moreover, projects involving public-private partnerships frequently offer attractive financial incentives, such as tax benefits and reduced regulatory hurdles, making them a favourable option for investors willing to diversify. The CMHC notes that affordable housing investments also benefit from steady demand, ensuring consistent rental income, even during economic downturns.Investors should consider the potential for benefits from nearby affordable or social housing projects, from infrastructure improvements to steady rental demand. In many cases, these projects do not lower property values and may even serve as catalysts for neighbourhood growth and investment returns. Thorough research and analysis are needed to accurately determine the impacts of specific social or affordable housing projects on an individual property or area.

Categories

Recent Posts