A Strategic Guide for GTA Homeowners Who Refuse to Be Left Behind

You Did Everything Right. So Why Are You Still Stuck?

You've watched your home appreciate for years. You've heard the headlines about Canada's housing crisis and "gentle densification." You've stood in your basement, or your backyard, and you've seen it — the second income suite, the in-law apartment, the laneway home — already finished in your mind.

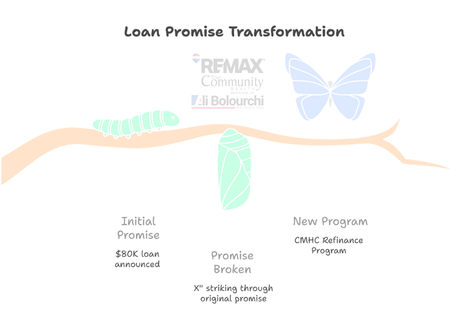

Then in 2024, the federal government handed you what looked like the final piece: the Canada Secondary Suite Loan Program. Up to $80,000. Just 2% interest. A 15-year term. You started pricing contractors. You called your accountant. You opened a folder labelled "Suite Project."

And then... silence.

No application portal. No instructions. No phone number that worked. By the time the 2025 federal budget was tabled, the program had been quietly cancelled — buried in a footnote, never having helped a single Canadian homeowner.

If that sounds familiar, here's what you need to know: You are not behind. You were misled by a program that never existed. And the real opportunity — the one that's actually moving GTA homeowners forward right now — was hiding behind it the entire time.

The Real Villain in Your Story

Most homeowners assume the villain is the market. Or interest rates. Or contractor prices.

It's not.

The villain is misinformation — the kind that keeps capable, financially healthy people frozen in research mode while their equity sits idle and their adult children sleep in childhood bedrooms.

The good news? The program that absorbed it — the CMHC Refinance Program — is, by nearly every measurable standard, more powerful than what was originally promised. You just have to know how to use it.

That's where this guide comes in.

Meet Your Plan: The CMHC Refinance Program

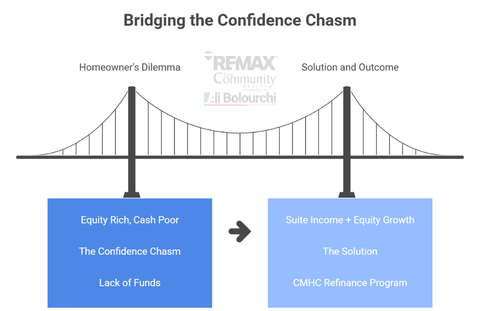

Here's what most homeowners don't realize. The CMHC Refinance Program doesn't just lend you money to build a suite. It lets you refinance against your home's future value — the value it will have after the suite is built.

Read that again.

You're not borrowing against what your home is worth today. You're borrowing against what it will be worth once the project is done — up to 90% of the post-construction value, capped at $2 million.

That single mechanic changes everything.

This is the bridge most Toronto homeowners didn't know existed.

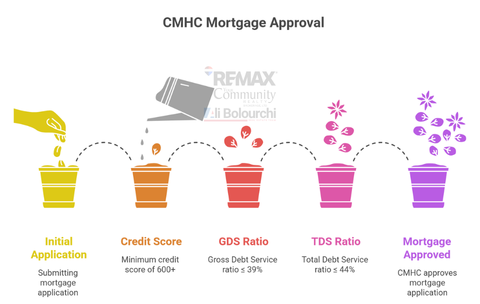

The Three Authority Signals: How Lenders Read You

Cialdini taught us that authority cuts both ways. The bank wants to know you are credible too. Under CMHC's framework, that credibility is measured by three numbers — and if you know them in advance, you can fix what needs fixing before you apply.

You also need to be a Canadian citizen, permanent resident, or non-permanent resident with valid work authorization — and you (or a spouse, common-law partner, parent, or child) must actually live in the home.

This is not a program for absentee investors. This is a program for people building a future on land they already stand on.

CMHC vs. Cash-Out Refinance: The Comparison Most Lenders Won't Make For You

Here's where most homeowners get quietly steered the wrong way. A traditional cash-out refinance is easier for a lender to process — so it's often the first option suggested. But for a secondary suite project, it's almost always the worse option.

CMHC vs. Cash-Out — The Honest Comparison

For a Toronto property where post-construction valuation can rise meaningfully — say, a Scarborough bungalow with a finished basement suite, or an East York semi with a laneway home — that 10% gap between 80% and 90% can be the difference between "someday" and "this year."

The 5-Step Plan: From Idea to Approval

This is where most articles end. This is where the real work begins. Here is the plan, in the order it actually happens.

A few things worth absorbing:

CMHC must approve the financing before construction starts. This is non-negotiable. Build first and you forfeit the program entirely.

Funds advance in stages. Not all at once. As each phase of the build is completed, the next tranche releases. This protects everyone — including you.

Not every lender is approved. Many mortgage brokers don't even mention this program because they don't have the relationships to execute it. The right professional makes this fast. The wrong one stalls you for months.

What Your Suite Must Be (and What It Cannot Be)

The suite has to qualify as a true secondary residence. That means:

A separate kitchen. Not a kitchenette. Not a microwave on a counter.

A separate bathroom. Full, functional, private.

A distinct living space. Suitable for full-time, year-round occupancy.

A private entrance. Independent access, separate from the main home.

Compliant with local bylaws and Ontario building code. Every line.

Rented for a minimum of 90 consecutive days if you choose to rent it. No short-term rentals. No Airbnb. No exceptions.

If your plan was to build a suite and rent it on Airbnb, this program is not for you. If your plan was to build something a parent, a child, or a long-term tenant could call home — this program was practically written for you.

The Cost of Waiting (And Why Smart Owners Are Moving Now)

Brian Tracy taught a principle that I think about often: the law of correspondence. What's happening on the inside — the hesitation, the second-guessing, the "I'll look into it next quarter" — almost always matches what shows up on the outside: equity sitting idle, family arrangements unsolved, opportunities passing.

Here is the honest math of waiting in 2026:

Construction costs in the GTA are still climbing, roughly 4–6% annually. The suite that costs $180K today is closer to $190K next year.

Mortgage rates remain volatile. The window for a favourable refinance is not permanent.

Municipal permitting timelines have lengthened, particularly for laneway and garden suites in Toronto. The earlier you start the paper trail, the earlier you finish.

Rental demand in the GTA continues to compress vacancy rates. Every month your suite isn't built is a month of foregone income.

The homeowners who started planning in late 2025 are pouring foundations now. The ones who waited for "more clarity" are still researching.

The Truth About Going It Alone

You can absolutely manage this process yourself. Many homeowners do. But understand what that means: you'll need to identify a CMHC-approved lender, coordinate two appraisals, manage permit timelines, vet contractors, structure the financing, and ensure every document aligns with CMHC's specific requirements — all while still working your full-time job and running your household.

Or, you can work with a Toronto real estate professional who has done this dozens of times — who knows which lenders move quickly, which contractors specialize in secondary suites, which neighbourhoods are seeing the strongest post-construction valuations, and which permit pathways are currently the fastest.

The choice isn't between "expensive" and "cheap." The choice is between months of confusion and a clear path forward.

Your Next Move

You came to this article looking for clarity on a federal program that no longer exists. You're leaving with something better: a working knowledge of the program that does, the framework to qualify, and the plan to execute.

But information alone doesn't build a suite. Action does.

🔑 Book Your 2026 Secondary Suite Strategy Session

A private, no-obligation 30-minute consultation where we will:

✅ Review your specific GTA property and its post-construction potential

✅ Identify the right financing path (CMHC, HELOC, or hybrid) for your numbers

✅ Connect you with a CMHC-approved lender who actually knows this program

✅ Map out a realistic 90-day action plan you can start this week

Spaces are limited to 6 consultations per month so I can give each property the deep attention it deserves.

[ → BOOK MY SECONDARY SUITE STRATEGY SESSION ]